Trade and technology

Small and medium-sized global traders are banking on blockchain

Published 18 July 2019

Eighty percent of all global trade is transacted through third-party lenders and cargo insurers. Blockchain has the potential to transform the trade finance process, which in turn could expand the supply of credit available for SMEs.

This is the second in a three-part series by Christine McDaniel on how blockchain technologies will play an increasing role in international trade.

Give me some credit

Every business requires capital to operate. To sell products to customers overseas, many companies also need trade financing and insurance from third-party lenders. About 80 percent of all global trade is transacted through third-party lenders and cargo insurers, but the process is complex, can be costly and many banks find it too risky to support small and medium-sized enterprises (SMEs).

Blockchain has the potential to increase transparency, speed and accuracy in assessing risk across the trade finance process, which in turn could expand the supply of credit available for international trade transactions – good news especially for SMEs that face significant hurdles accessing credit. Here’s how.

Pay me now or pay me later

Buyers who import goods from sellers in other countries generally want to pay upon receiving the merchandise so they can verify its physical integrity on arrival. Exporters, on the other hand, generally prefer to be paid as soon as they ship the goods. Trade finance can bridge this gap.

Exporters and importers engage third-party lenders and insurers who will guarantee payments on the basis of collateral and indemnify the exporter, importer and related parties in the event that the merchandise is damaged, stolen or lost while in transit. In this way, trade finance provides the credit, payment guarantee and insurance needed to facilitate an international trade transaction on terms that will satisfy all parties.

Steps on the trade journey

Intermediaries such as freight forwarders typically manage the physical journey of merchandise, from the original producer to the border, across the border (maybe several borders), and to the final buyer.

Each step must be verified: when was the merchandise transported from the factory or farm to a warehouse, when was it moved from the warehouse to a container, when was the container loaded onto a ship, when did the ship get underway, when was the container unloaded from the ship at port, and when was the merchandise transported from the port to the end consumer.

Different trade finance instruments, such as lending, letters of credit, factoring and cargo insurance cover legs of the journey. A letter of credit is a guarantee from a bank that a buyer’s payment will be received and be on time or else the bank will take responsibility for the payment. Factoring is accounts receivable financing to accelerate cash flow. Cargo insurance insures the merchandise while en route.

Without finance, trade would sink

The World Trade Organization estimates that 80 percent of global trade relies on trade finance or credit insurance. The global trade finance sector (i.e., the global volume of letters of credit) is worth roughly US$2.8 trillion. Demand for trade financing exceeds availability, resulting in the underutilization of existing capital. According to the Asian Development Bank, the global trade finance gap — the difference between the demand for and supply of trade finance — has reached US$1.6 trillion.

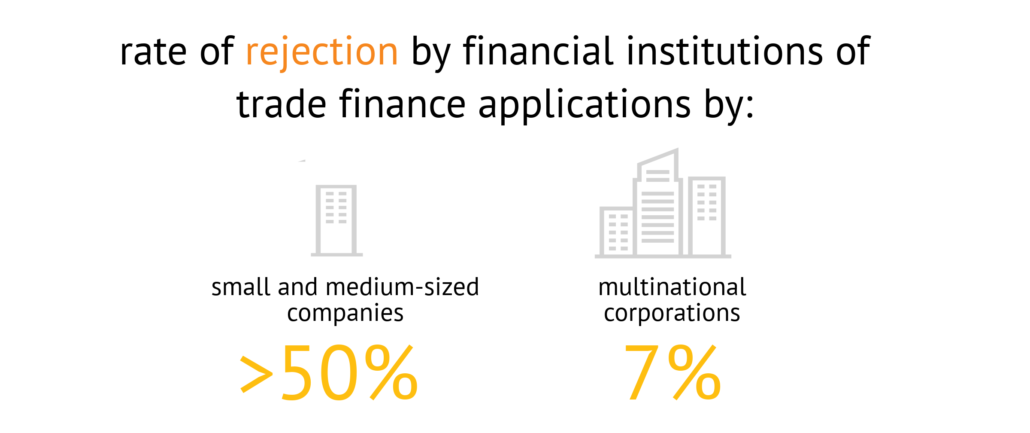

SMEs face a 50 percent rejection rate

The shortfall in supply reflects the complex and risky nature of trade finance which often involves multiple parties. Before banks will issue letters of credit in trade finance, they require potential customers to present a solid credit history and a strong balance sheet, conditions that tend to favor larger institutions.

SMEs typically experience more difficulty navigating the trade finance process and dealing with the cost and complexity of banking regulations than larger companies. In 2014, SMEs had trade finance requests before financial institutions rejected at a rate of over 50 percent. In comparison, the rejection rate for multinational corporations was only seven percent.

Links in the trade finance chain

According to the United Nations, there are typically eight major steps required to obtain a letter of credit, although in practice the Credit Research Foundation lists more than twenty. Each step of the process is dependent on the previous steps, and some steps involve sending the same document back and forth for verification purposes. The administrative burden is greater for SMEs than for large firms.

A survey of 2,350 SMEs and 850 large firms conducted by the U.S. International Trade Commission in 2010 showed that lack of access to credit is the major constraint for SME manufacturing firms seeking to export or expand into new markets and it is one of the top three constraints for SME services firms.

How blockchain can help ease trade finance

Requirements to authenticate each transaction in the trade finance and insurance process can engender large amounts of paperwork and cause delays at each step. Every handoff must be approved and verified.

Instead, blockchain uses digital tokens that are issued by each participant in the supply chain to authenticate the movement of goods. Every time the item changes hands, the token moves in lockstep. The real-world chain of custody is mirrored by a chain of transactions recorded in the blockchain.

The token acts as a virtual “certificate of authenticity” that is much harder to steal, forge or hack than a piece of paper, barcode or digital file. The records can be trusted and greatly improve the information available to assure supply-chain quality.

Using blockchain as a digital ledger for these handoffs would allow involved parties to instantly track and receive secure information about the traded goods. Parties can monitor the entire shipping process and verify the completion of each step in real time. This increased transparency and ease of monitoring reduces the risk that a borrower presents to a potential lender or insurer.

Banking on blockchain

A number of financial institutions are piloting the use of blockchain-enabled trade finance platforms.

Bank of America, HSBC, and the Infocomm Development Authority of Singapore collaborated in 2016 to develop a trade finance application designed “to streamline the manual processing of import/export documentation, improve security by reducing errors, increase convenience for all parties through mobile interaction, and make companies’ working capital more predictable.” Using the application, each action in the workflow is captured in a distributed ledger and all parties (the exporter, the importer, and their respective banks) can visualize data in real time, offering transparency to authorized participants while ensuring confidential data is protected through encryption.

Barclays used blockchain in 2017 to issue letter of credit that reportedly guaranteed the export of $100,000 worth of agricultural products from Irish cooperative Ornua to the Seychelles Trading Company, noting the parties were able to execute a deal in four hours that would usually take up to 10 days to complete.

A group of European banks launched a trade finance blockchain platform in July 2018, initially focused on facilitating small and medium-sized businesses trading within Europe. In September 2018, the Hong Kong Monetary Authority announced plans to launch a trade finance blockchain platform. Twenty-one banks are participating in the platform, including large institutions such as HSBC and Standard Chartered. The Hong Kong Monetary Authority is also reportedly working with its counterpart in Singapore to develop a blockchain-based trade finance network to settle cross-border transactions.

Lessons for trade policymakers

As the trade finance industry begins to utilize blockchain technology, there are some potential implications worthy of policymakers’ attention.

First, the large number of intermediaries and corresponding administrative costs in trade finance tend to fall particularly hard on SMEs and the relatively higher cost of each transaction makes SME financing less attractive to banks. If blockchain can reduce the costs of trade finance, more small and medium-sized businesses could trade globally.

Second, although blockchain technology does not alter the fundamental credit risk of borrowers, the increased transparency and access to information it delivers could improve the accuracy of banks’ risk assessments. If perceived risk is greater than actual risk, a nontrivial number of loan applications may be denied even though those loans have the potential to be successful. If blockchain brings greater confidence and issuance of good loans — that is, those that are paid back — the transactions they support would bring value to the economy.

In these important ways, blockchain can increase transparency across the trade finance process and decrease risk for all parties, in turn expanding the supply of credit available for international trade transactions.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).

Author

Christine McDaniel

Christine McDaniel is a senior research fellow with the Mercatus Center at George Mason University.

Have any feedback on this article?

Related articles