Trade and technology

Understanding how China secured its chip stack

Published 08 April 2025

In March 2025, a team from Peking University made waves when it announced an achievement that shattered semiconductor performance limits – without using silicon. The breakthrough, on the heels of DeepSeek, underscores China’s tech innovative capacity, undeterred by America’s tech denial strategy. Developing an effective policy campaign to preserve the West’s lead in high-end tech demands a far more robust understanding of China’s current positioning and priorities.

Semiconductors are essential for all technologies and are inherently dual-use. Their production process is comprised of three main steps: Design, fabrication, and assembly. Every step requires its own set of technological, equipment, and chemical and material inputs. No single country possesses every element of the semiconductor production stack, relying instead on a multi-step global value chain integrating the US, Taiwan, South Korea, Japan, Europe, and China. While this global division of labor is efficient, it introduces resilience concerns and geopolitical risks. For instance, Taiwan's critical role in the semiconductor supply chain, particularly through TSMC, presents a single point of geographic failure that could shut down the world overnight.

Beijing has long prioritized resolving the risks posed by foreign dependence in the semiconductor value chain and – as part of a larger industrial offensive oriented around securing asymmetric international leverage over strategic industries – has sought both to secure indigenous domestic capabilities across the value chain and to shore up nodes of absolute global dominance. Beijing had laid out its plan on this as early as 2006, in the National Medium- and Long-Term Science and Technology Development Plan Outline issued by the State Council.

Download Understanding how China secured its chip stack by Nathan Picarsic and Emily de la Bruyère:

In recent years, the US and its allies have begun to make corresponding investments in securing domestic semiconductor production capability, such as the CHIPS and Science Act. On the defensive side, Washington has drastically expanded export controls on the flow of US-generated and -controlled technology to China. Despite US government interventions, Beijing has only continued to expand its capabilities and leverage. The global semiconductor layout has a dangerous reliance on China hardwired into it. And US government efforts thus far have not changed that.

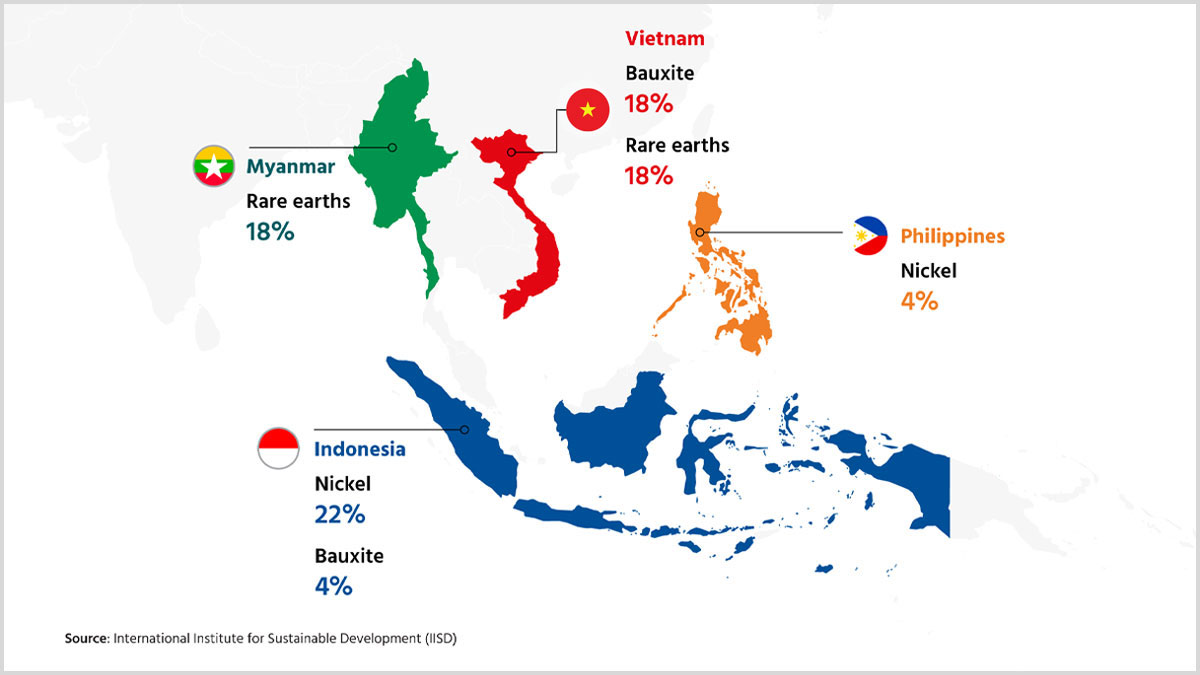

At a surface level, the United States appears to lead the international semiconductor industry with major brands like Intel, Micron, and Qualcomm. However, this downstream leadership masks significant dependencies. US semiconductor champions depend on Chinese production, testing, and packaging, as well as downstream electronics product assembly. This grants Beijing the ability to disrupt US operations and influence boardrooms. China also holds a dominant position in the production and processing of a wide range of semiconductor-relevant raw materials, including gallium, germanium, magnesium, natural graphite, scandium, tungsten, and the entire range of rare earth elements.

Furthermore, Beijing is adept at identifying growth areas like data centers and artificial intelligence. It emphasizes the production of third-generation chips made with gallium nitride, silicon carbide, and indium phosphide. Compared to traditional silicon semiconductors, third-generation chips can handle higher power, temperatures, and voltages, making them well-suited for electric vehicles, data centers, and renewable energy generation. China’s emphasis on third-generation semiconductors has yielded domestic champions in the field, like Zhongji Innolight – the world’s leading provider of optical module solutions, small hardware that helps to network data centers and transmit high-throughput data flows that propel cutting-edge AI applications. So far, the likes of this field are well below the radar of US "chip war" discussions, presenting Beijing with a leapfrog opportunity. It threatens both to exacerbate and lock in global dependence on Chinese semiconductor inputs in some of today’s hottest technological and industrial domains.

At present, the US does not sufficiently understand how China positions itself in the global semiconductor value chain, what China is doing, or to what end. Rather, Washington assumes that Beijing and its corporates approach the technological contest the same way that the US and its private sector do; that challenges will be symmetric; that the two sides are running in the same direction in a straightforward race. If the US can better understand China’s capabilities and positioning, it will conclude that the current semiconductor contest is not simply one for the cutting-edge of the value chain’s downstream. Rather, Beijing is competing for the entire value chain. Beijing is also competing to scale relatively proven technologies and processes that have clear market demand and, in many cases, a relatively low profit margin that decreases overall competition and allows China to cement a monopoly.

The challenge China presents is too big to be addressed by the sort of direct subsidies and grants laid out in recent initiatives like the CHIPS Act. Washington should instead focus on increasing the costs of dependence on China, for inputs or for sales, such that capital is incentivized to support US and other trusted alternatives. The US already has the toolkit to do this, including tariffs and import restrictions that have been deployed. But Washington needs better enforcement of this toolkit, in addition to working with US partners and investing in upstream inputs of the semiconductor value chain. The next chapter of US tech policy should center on building a robust domestic and international trade system protected from China's distortions.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).

Author

Nathan Picarsic

Nate Picarsic is a co-founder of Horizon Advisory, a leading geopolitical and supply chain intelligence provider.

Have any feedback on this article?

Author

Emily de la Bruyère

Emily de La Bruyère is a senior fellow at the Foundation for Defense of Democracies (FDD), and co-founder of Horizon Advisory, a strategic consultancy focused on the implications of China’s competitive approach to geopolitics.

Have any feedback on this article?

Related Articles