Published 05 November 2024

When it comes to securing supply for critical minerals it does not possess in sufficient quantities at home, China has been investing heavily overseas. In Southeast Asia, Beijing has invested about US$4 billion since 2012 in 12 projects, a lot of it concentrated in Indonesia, which exports 16% of the world’s nickel. From a long-term geopolitical, economic, and sustainability perspective, it is not in ASEAN’s interests to be drawn exclusively into one Great Power’s sphere of influence.

In 1992, Deng Xiaoping quipped that the Middle East might have oil, but China had rare earths. China’s industrial growth in the past 40 years has required the import of large amounts of minerals, but this took place against the backdrop of acute state awareness on the need to secure supply.

China’s approach to supply security has multiple prongs. China has nurtured its own extractive industries to ensure its domestic reserves are well utilized. This has entailed a degree of light-touch health, safety, and environmental oversight that has lowered production costs relative to other parts of the world, which has triggered criticism from other economies on China’s use of state-controlled economic levers for geostrategic purposes at the expense of the rest of the world. Chinese companies operating in the critical minerals space have enjoyed significant industrial subsidies, and Beijing has also invested heavily in stockpiling where it considers its supplies to be vulnerable.

When it comes to securing supply for minerals China does not possess in sufficient quantities at home, China has been investing heavily overseas. According to the fDi Markets database of Chinese outbound greenfield investment, there have been 124 investments in the extraction sector since 2003 with a total value of about US$66 billion. Of these, 91 projects with a value of about US$48 billion have been in the metals and minerals sector, suggesting that securing metal and mineral supplies has been a higher priority than hydrocarbons.

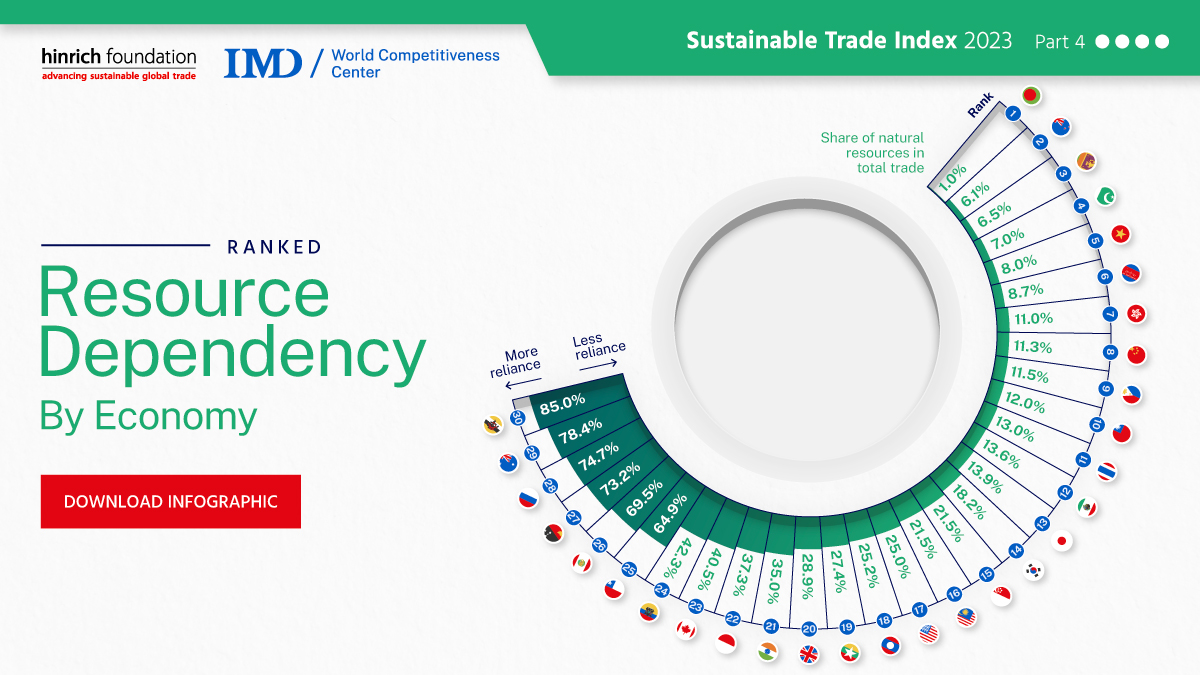

Download China’s long shadow on critical minerals looms over Asia by Stewart Paterson:

Southeast Asia is home to some of the largest deposits of critical minerals in the world. The region has about 26% of global reserves of nickel. Indonesia has the bulk, with 22% and the Philippines with 4%. Vietnam and Myanmar are thought to have about 18% of global rare earths reserves each. Between 2012 and 2023, China’s share of ASEAN exports of nickel has risen from 3% to 62%, aluminum from 5% to 21%, copper from 15% to 32%, and iron from 4% to 40%.

According to fDi Markets, Indonesia has been the recipient of no less than US$36 billion of FDI from China in the metals industry. This influx of Chinese FDI has accelerated since Indonesia banned the export of raw nickel ore and has brought unintended consequences. Domestic miners, unable to export, had no choice but to sell nickel domestically to Chinese-owned processors at below-market prices. There is also a risk that the rapid growth in nickel processing and value-added capacity is pressuring producers to over-exploit nickel reserves in a way that will significantly shorten the lifespan of the resource. Furthermore, the environmental impact of the rapid growth of the industry has induced significant push-back from local communities despite the economic benefits.

The fact that the EU and the US are keen to secure supplies of critical minerals to facilitate catching up with China presents an opportunity for Southeast Asian countries to negotiate long term supply contracts that limit key risks in the industry, writes Senior Research Fellow Stewart Paterson in this paper. Handled well, this should enable ASEAN member states to participate more fully in supply chains. It will also enable ASEAN member states to balance their trade and investment relationships with major global powers in a way that reinforces their own agency and sovereignty.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).

Stewart Paterson is a Senior Research Fellow at the Hinrich Foundation who spent 25 years in capital markets as an equity researcher, strategist and fund manager, working for Credit Suisse, CLSA and most recently, as a Partner and Portfolio Manager of Tiburon Partners LLP.

Have any feedback on this article?

Related Articles